Selling a valuable asset that has appreciated allows investors to receive a return. Unfortunately, selling an appreciated asset also means paying capital gains tax on that appreciation. Depending on the sale price, an owner may face a hefty tax bill in the year of the sale. Using a deferred sales trust in conjunction with an asset sale can help owners manage or minimize tax liabilities from the sale.

However, a deferred sales trust must meet specific requirements for an asset owner to legally defer taxes from a sale. As a result, working with an experienced deferred sales trust lawyer can help you receive the benefits of setting up a trust. Contact Pennington Law, PLLC, today for a consultation to discuss your situation.

What is the Purpose of a Deferred Sales Trust (DST)?

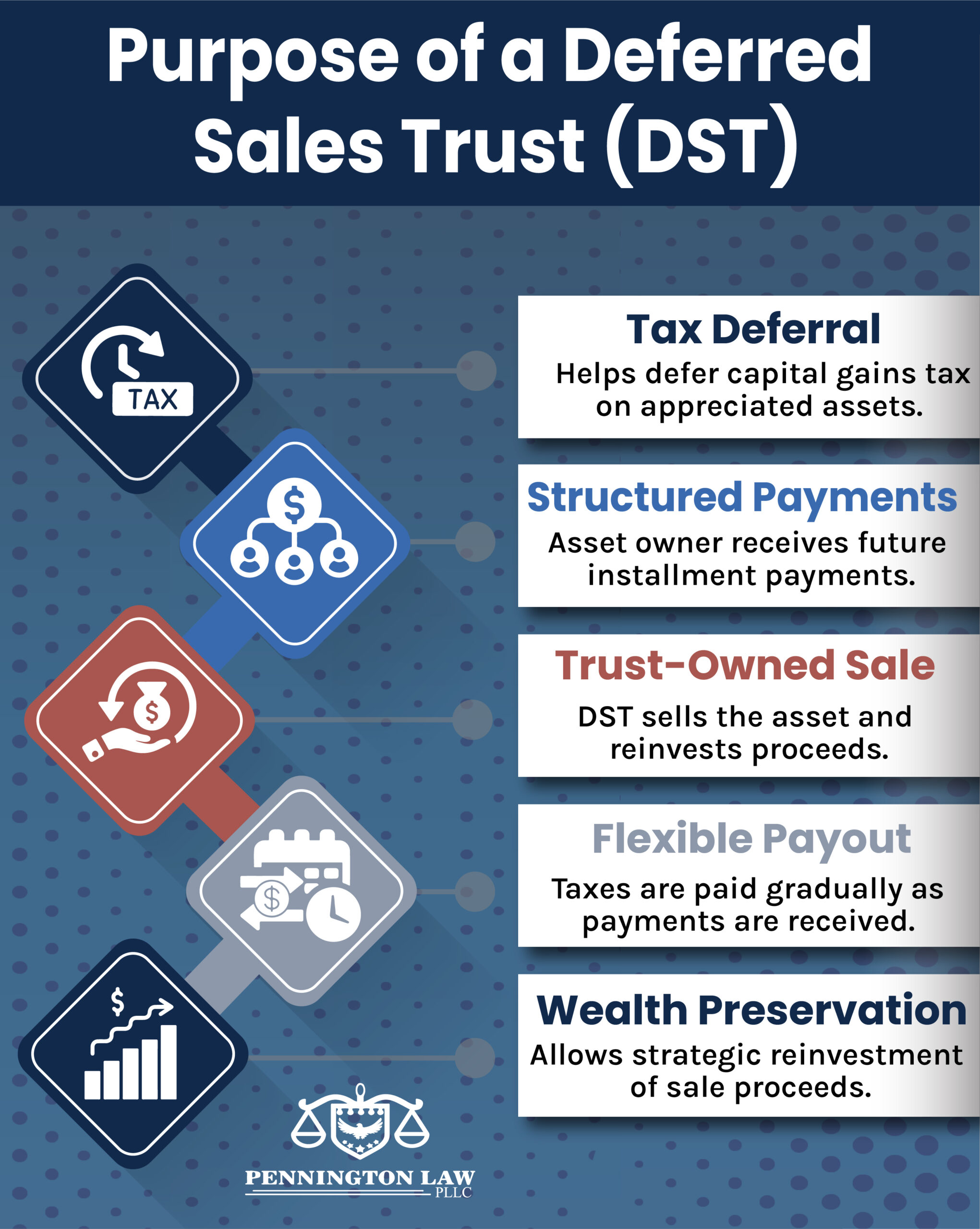

So, what is a deferred sales trust (DST)? It’s something that can offer people a means of deferring capital gains tax liability when selling appreciated assets.

An asset owner sells their asset to the DST in exchange for the promise of future installment payments, as defined by an installment note or installment payment contract between the trust and the asset owner. The trust then sells the asset and invests the proceeds to pay the original asset owner per the installment agreement.

When set up correctly, a DST allows an asset owner to pay taxes as they receive payments from the trust rather than paying capital gains tax upfront upon selling the asset.

Who Can Benefit from Setting Up a Deferred Sales Trust?

A person may benefit from setting up a deferred sales trust if they expect to incur a significant tax liability upon selling an asset that has appreciated during their ownership, such as real estate, investments, or a business interest.

An asset owner considering a sale of an asset may benefit from using a DST rather than another option for deferring taxes, such as a Section 1031 exchange, if the owner does want to meet the requirements of a 1031 exchange (including acquiring other property of like-kind from the sale proceeds). DSTs used in estate planning can benefit families by helping heirs manage tax liability from their inheritances.

How Do I Set Up a DST?

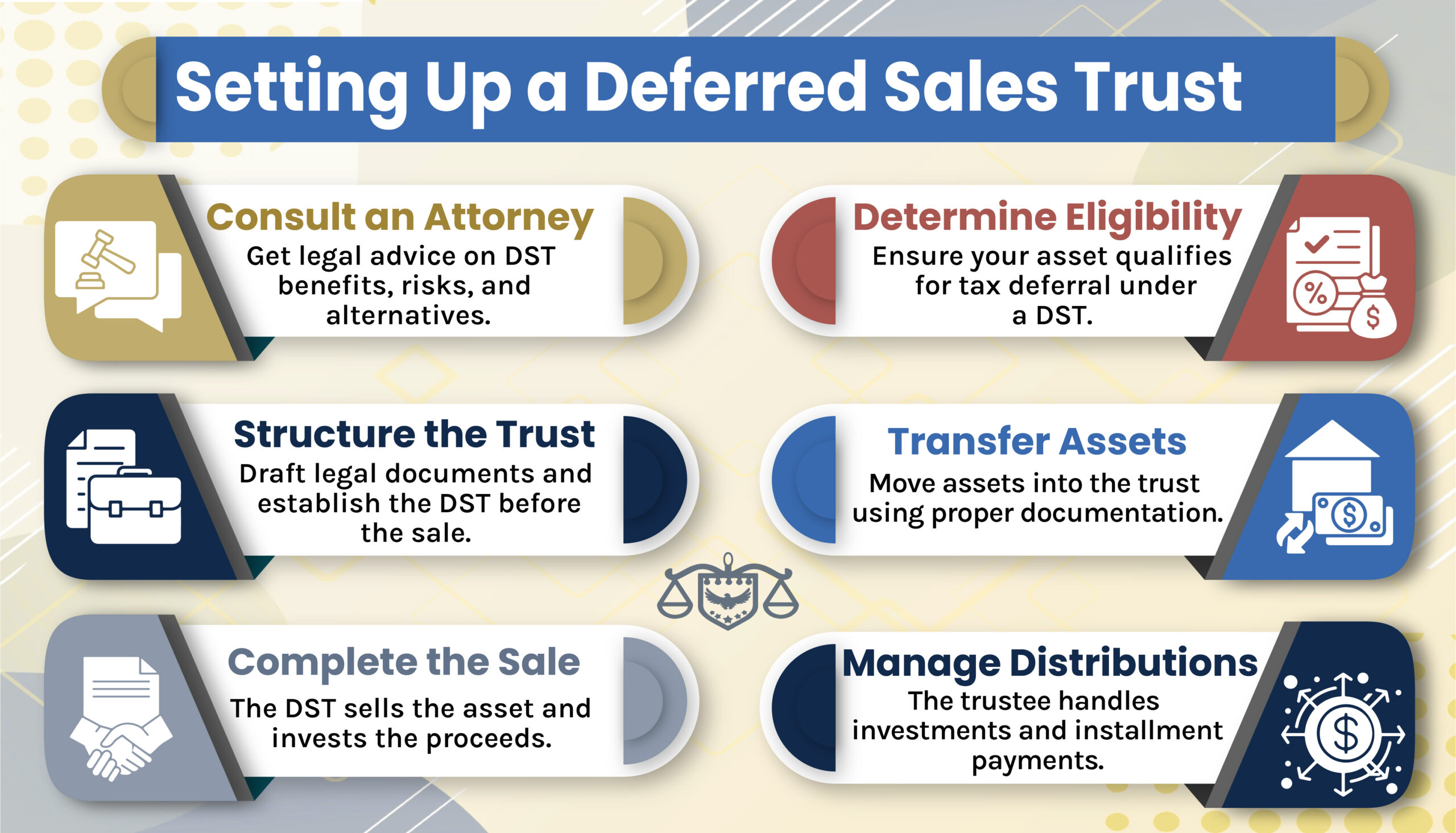

Setting up a deferred sales trust in Arizona involves several steps:

- Consult an Arizona Estate Planning Attorney – A deferred sales trust attorney can help you understand how DSTs work and the pros and cons of using a DST in conjunction with an asset sale and walk you through alternatives to using a DST for tax and estate planning purposes.

- Determine Eligibility for a Deferred Sales Trust – An attorney can also help you evaluate the suitability of a DST for your situation, including whether applicable tax laws will allow you to defer tax liabilities for an asset sale through a DST.

- Structure the Trust – Your attorney can help you complete the paperwork needed to structure the trust, including drafting and executing the trust document and the installment payment agreement between yourself and the trust. Applicable laws and regulations require you to structure the trust expressly as a DST and form it in advance of closing on the sale of the asset or the applicable tax trigger date.

- Transfer the Assets into the Trust – An attorney can also assist you with transferring the asset(s) into the trust, including executing necessary paperwork like deeds or title transfers.

- Execute the Sale Through the Trust – Once you’ve transferred the asset to the DST, the trust can execute the sale with the purchaser and receive and invest the sale proceeds.

- Manage and Benefit from the Trust – After the sale, the person or company you’ve appointed to serve as trustee of the DST can manage and invest the sale proceeds and distribute income and principal as required by the installment payment agreement.

Advantages and Disadvantages of a Deferred Sales Trust

Before you commit to setting up a deferred sales trust, it’s smart to familiarize yourself with some key deferred sales trust pros and cons.

DST Pros

Some of the benefits of DSTs include the following:

- A DST allows a property owner to defer capital gains taxes from selling the asset over multiple years since the owner pays taxes only upon receiving payment of principal from the sale proceeds from the trust.

- Because taxes only come due upon receiving payment from the principal of the sale proceeds, a person may defer capital gains taxes indefinitely by structuring a DST to pay income only from the invested sale proceeds, keeping the principal in the trust.

- DSTs avoid many trickier requirements of other tax-deferred structures, such as the “like-kind” requirement of a 1031 exchange.

- Families can use DSTs to avoid probating high-value assets and minimize tax liabilities for heirs by paying them income from the trust.

DST Cons

However, DSTs have some downsides that asset owners should consider before setting up a DST, including:

- DSTs can have high setup and management fees, which may reduce the income available for payment.

- An asset owner must give up ownership of the asset by transferring it to the trust. Furthermore, through the installment payment agreement, they do not become a beneficiary but a creditor. As a result, the owner will have less control over the trust than a beneficiary might.

- When the owner structures the trust to invest the asset sale proceeds, the owner accepts the risk of investment loss, which can adversely affect the amount and timing of payments under the installment agreement.

- DSTs lose some of their tax advantages when the face value of the installment agreement reaches a certain threshold, as owners may have to pay interest on the deferred tax attributable to amounts over that threshold.

Frequently Asked Questions About Deferred Sales Trusts

At Pennington Law, PLLC, we receive numerous questions about deferred sales trusts, as many clients are unfamiliar with what they are and how they operate. Here are some of the common questions we hear:

What timeline should you follow for the DST process?

The timing of a deferred sales trust is crucial, particularly in relation to the closing date of your asset sale. A DST must be fully established before the sale closes. This means you should finalize the trust documents and installment agreement in advance. If the asset transfers directly to the buyer before the DST is in place, you may lose the opportunity to defer capital gains taxes.

For this reason, many people start working with an attorney early in the negotiation stage of a transaction. Preparing the trust before closing allows for a seamless transfer of the asset into the DST, followed by the sale to the buyer. Planning the timeline carefully also reduces the risk of administrative mistakes that could invalidate the tax treatment. In short, don’t wait until closing is imminent — address the deferred sales trust structure as soon as you anticipate a sale.

What is the difference between a 1031 exchange and a deferred sales trust?

A 1031 exchange and a deferred sales trust are both tools for managing capital gains taxes, but they work in very different ways. A 1031 exchange enables property owners to defer taxes by reinvesting sale proceeds in a like-kind property, subject to strict deadlines and requirements. If you cannot or do not want to purchase another property, a 1031 exchange may not be a good fit.

By contrast, a deferred sales trust does not require the purchase of new property. Instead, the asset is transferred into a trust, sold, and the proceeds invested according to the terms of the installment contract. The trust then makes payments back to the seller over time, spreading out tax liability. For many people, DSTs offer greater flexibility than 1031 exchanges because the proceeds can be invested in a broader range of assets, not just real estate.

What is the IRS position on a deferred sales trust?

The framework for DSTs is built on existing tax law regarding installment sales under Section 453 of the Internal Revenue Code. When appropriately structured, a DST operates within these installment sale rules. That means the IRS generally recognizes the deferral of capital gains taxes as long as the transaction follows Section 453 requirements.

However, the IRS may closely scrutinize DSTs that are poorly drafted, improperly managed, or marketed with unrealistic promises. This makes it essential to work with legal and tax professionals who understand how to design and administer a DST that complies with tax regulations. While no strategy is entirely risk-free, a carefully prepared DST that follows established tax principles has support in existing law.

Talk to an Arizona Trust Attorney for Help With Your Estate Plan

![]() When you wish to sell a valuable asset, such as real estate, intellectual property, or a business ownership interest, a deferred sales trust can help you and your family manage capital gains tax liability arising from the sale.

When you wish to sell a valuable asset, such as real estate, intellectual property, or a business ownership interest, a deferred sales trust can help you and your family manage capital gains tax liability arising from the sale.

Contact Pennington Law, PLLC today to discuss the suitability of using a DST as part of your transaction and to receive help in structuring a valid and enforceable trust. The first consultation is free.