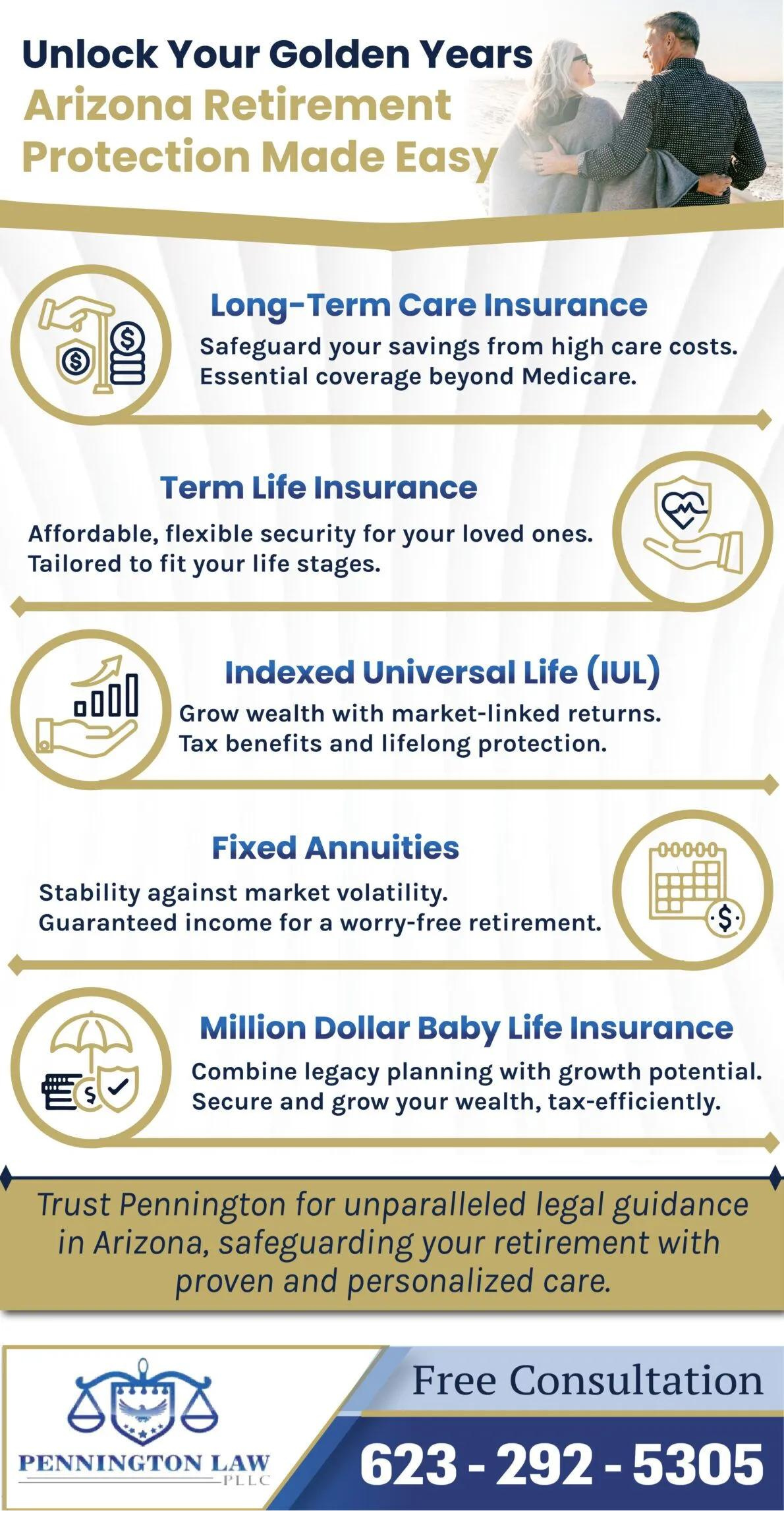

Looking toward retirement is exciting, but financially preparing for it can also be stressful. To ensure you can enjoy your golden years to their fullest, you should consider the different types of products available, such as long-term care insurance, annuities, and different types of life insurance policies.

Andre L. Pennington, an experienced financial professional, can review your options and help you safeguard your future. Contact Pennington Wealth, PLLC today for a free and confidential consultation with a retirement protection professional in West Valley Arizona. We serve clients in Buckeye, Sun City West, Surprise, and Peoria.

What Is Long-Term Care Insurance?

Long-term care (LTC) insurance covers the costs of things like nursing homes, in-home caregivers, and assisted living. According to Consumer Affairs, a recent study showed that the median cost of a semi-private room in a nursing home in the United States was $7,756 per month. The study also found that the median for a private room in a nursing home was $8,821 per month.

As you can see, long-term care can be expensive, and, unfortunately, health insurance does not usually cover the cost of these necessary living arrangements and services. As a result, having the right long-term care insurance can protect your retirement savings while getting the help you need to live as long and as independently as possible.

To consult with an experienced retirement planning attorney serving West Valley Arizona, call 623-292-5305

Proper planning can take the fear out of retirement and allow you to focus entirely on its many rewards. The sooner you begin preparing, the sooner you can have peace of mind. Reach out to Pennington Wealth, PLLC today to speak with Andre L. Pennington, a reputable retirement protection professional in West Valley Arizona.

Proper planning can take the fear out of retirement and allow you to focus entirely on its many rewards. The sooner you begin preparing, the sooner you can have peace of mind. Reach out to Pennington Wealth, PLLC today to speak with Andre L. Pennington, a reputable retirement protection professional in West Valley Arizona.