When you have worked hard to create wealth, you may want to share it with others or pass it on to your loved ones. However, you might have concerns about giving large sums of money to a family member whose personal circumstances put them at risk of squandering their inheritance. For example, you might worry about a loved one suffering from addiction or who has negligent spending habits.

Fortunately, you have estate planning options that can allow you to protect your wealth as you pass it on to your loved ones. With a spendthrift trust, you can control the distribution of your legacy to your beneficiaries and heirs. A spendthrift trust attorney from Pennington Law, PLLC, can help you determine whether you need a trust in your estate plan.

Our legal team has extensive estate planning experience, counseling clients from various backgrounds. Our attorneys’ dedication to achieving optimal outcomes for our clients has earned our firm numerous awards and accolades, including top ratings from Super Lawyers and Best Attorneys of America, recognitions from Lawyers of Distinction and Elite Lawyers, Best Attorney in Sun City West 2021 by the Daily Independent, and Best Probate Attorneys in Surprise, Peoria, and Goodyear by Expertise.com.

Contact Pennington Law, PLLC, today for a free initial case evaluation to speak with a West Valley Arizona spendthrift trust lawyer about setting up a trust for your family. Our firm can help you better understand what spendthrift trusts do and advise whether this kind of trust might work for you. We serve clients in Surprise, Sun City West, Peoria, Buckeye, and the surrounding Arizona communities.

To consult with an experienced spendthrift trust attorney serving West Valley Arizona, call 623-292-5305

What Is a Spendthrift Trust?

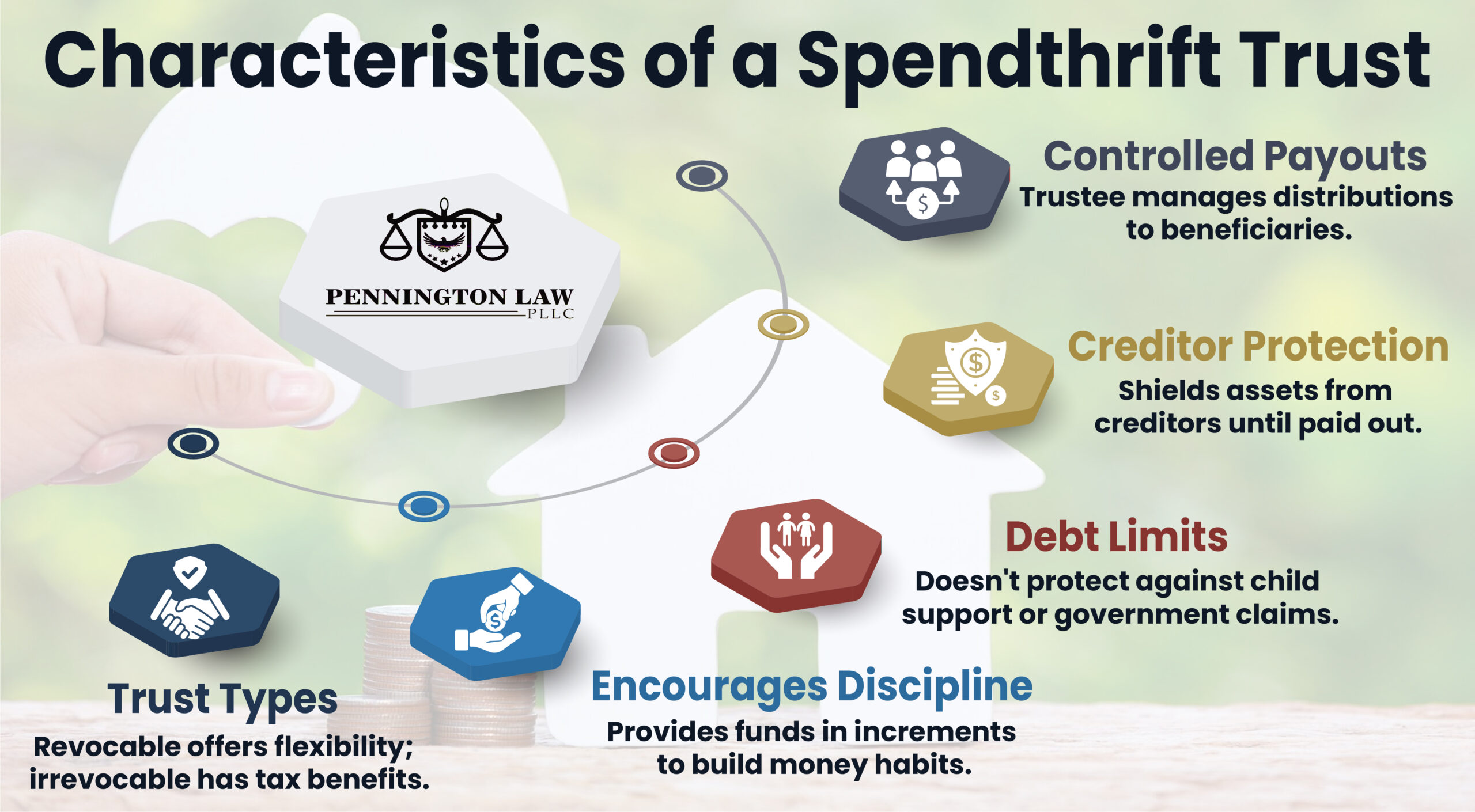

A spendthrift trust is a type of trust that limits the beneficiary’s access to income or trust principal. In a spendthrift trust, the trustee has the authority to distribute income or assets to the trust’s beneficiaries according to the spendthrift provisions.

What Are the Spendthrift Trust Laws in Arizona?

Under Arizona law, a spendthrift provision is valid only if it clearly restricts both the voluntary and involuntary transfer of a beneficiary’s interest. In practice, this means a beneficiary cannot sell, assign, or pledge their future trust distributions, and creditors cannot seize trust assets before the trustee releases them. The statute also clarifies that a trust is not automatically considered a spendthrift trust. The restriction must be written into the trust document in plain terms.

However, certain creditors still have a right to reach trust distributions, even when a spendthrift provision is in place. These exceptions to the spendthrift provision law include claims for child support, spousal maintenance, and restitution orders. In addition, the statute permits government claims, such as tax obligations, to attach to distributions. While most creditors must wait until the trustee releases funds to the beneficiary, these specific types of creditors can bypass some of the protections otherwise offered by the spendthrift clause.

Finally, state law also outlines the rights of creditors when a trustee makes discretionary distributions. If a trustee has discretion over whether or not to distribute funds, a beneficiary’s creditors cannot compel payment from the trust. However, once the trustee exercises discretion and distributes money, those funds may be subject to collection. This statute reinforces the protective nature of discretionary spendthrift trusts while confirming that distributions, once made, are generally fair game for creditors.

How Does a Spendthrift Trust Work?

Spendthrift trusts limit the beneficiary’s ability to sell or give away their interest in the trust. A beneficiary’s creditors cannot reach a spendthrift trust’s assets; they can only claim the money after the trustee distributes it to the beneficiary. However, the trust cannot avoid specific categories of debts, such as child or spousal support obligations or government claims, and liens can be placed on future distributions from the trust for those debts.

Spendthrift Trusts: An Example

For example, you can leave $100,000 to a loved one through a spendthrift trust to ensure the money remains safe and to encourage your loved one to learn good financial habits. The spendthrift trust can direct the trustee to release the $100,000 in regular increments, such as paying a few thousand dollars each month. If trust assets generate income, a spendthrift trust may direct the trustee only to pay the beneficiary the revenue generated. The beneficiary’s creditors may not touch any of the $100,000 of trust assets, nor can the beneficiary pledge future distributions to their creditors.

Is a Spendthrift Trust Irrevocable or Revocable?

A grantor can make a spendthrift trust revocable or irrevocable. A revocable trust refers to a trust where the grantor can change the terms of the trust during their lifetime, whereas a grantor cannot amend the terms of an irrevocable trust. Although revocable trusts can provide grantors with flexibility, irrevocable trusts often enjoy certain tax advantages that revocable trusts do not.

Arizona spendthrift trust attorney near me

When Is a Spendthrift Trust Typically Used?

You might use a spendthrift trust as part of your estate plan in certain circumstances, such as:

- You wish to give or bequeath money to a loved one with poor financial habits, and you have concerns that they might squander the money you give.

- You want to give money to a beneficiary with substantial debt and protect your gift from the beneficiary’s creditors.

- The beneficiary suffers from drug, alcohol, or gambling addictions that might cause them to squander the money.

- You give or bequeath money to a vulnerable loved one or a loved one who might fall prey to scammers.

- You want to distribute an inheritance incrementally, especially if you have children still in childhood or young adulthood who have yet to learn good money management practices.

- You want to refrain from having the beneficiary take ownership of the assets for other financial reasons, such as maintaining their eligibility for government benefits.

How Much Control Does a Trustee Have Over a Spendthrift Trust?

The trustee must safeguard the trust assets and distribute them to the beneficiary according to the terms of the spendthrift trust. A trustee has as much control and discretion over a spendthrift trust as the grantor provides under the terms of the trust.

A grantor may impose specific limitations on a trustee’s authority or grant the trustee discretion over the trust’s operation. The control given to the trustee should reflect the grantor’s particular concerns for the beneficiary and the goals of the spendthrift trust.

Aspects of the trustee’s powers that the grantor can limit include:

- When the beneficiary can begin receiving distributions, such as after graduating from college or reaching a certain age

- How often the beneficiary receives payouts, such as on a monthly or quarterly basis

- How much money the trustee can distribute, including limiting the trustee to only distributing the trust’s income or indexing payments to inflation

- Whether the trustee can make distributions to pay for certain expenses incurred by the beneficiary

- Whether the trustee can make emergency distributions from trust income or principal

- Whether the trustee should pay for the beneficiary’s expenses rather than simply disbursing money to the beneficiary

- Whether the trustee can refrain from making distributions based on the beneficiary’s behavior, including pausing payments if the beneficiary becomes addicted to drugs, gambles heavily, or does any other activity that might put them at risk of spending irresponsibly

Alternatively, the grantor can give the trustee the authority to exercise discretion over when to disburse money from the trust and how much money to distribute to beneficiaries.

In many spendthrift trusts, the grantor will name themselves trustees to watch over and protect their loved one who benefits from the trust. However, the grantor should also nominate a successor trustee to manage the trust after the grantor’s death. A trustee can receive compensation for their services to the trust but may not use trust assets for their personal benefit.

Click to contact our West Valley Arizona spendthrift trust lawyer today

What Are the Advantages of a Spendthrift Trust?

A spendthrift trust can provide grantors with the advantage of ensuring that their wealth will benefit their loved ones for a long time. Some of the critical benefits of spendthrift trusts include the following:

- Disbursing payments in an incremental manner rather than all at once, which can help the beneficiary learn money management over time or avoid the shock of receiving a large inheritance

- Protecting your estate from your beneficiary’s poor financial habits, as the beneficiary only receives incremental payments rather than having access to the entire amount of the trust at once

- Protecting the money you give from your beneficiary’s creditors, as most creditors cannot bring claims against the trust to collect on the beneficiary’s debt

- Bypassing the probate process if you want to use the spendthrift trust to give an inheritance to loved ones

- Providing for a vulnerable loved one suffering from mental or cognitive disabilities or addictions

- Preserve a vulnerable loved one’s eligibility for government benefits, because the trust owns the assets on behalf of the beneficiary

What Are the Drawbacks of a Spendthrift Trust?

Although spendthrift trusts provide valuable protections, they are not without limitations. Families considering this type of trust should familiarize themselves with these potential disadvantages before making it part of their estate plan:

- Legal and administrative costs to create and maintain the trust

- Loss of flexibility if the trust is irrevocable

- Potential conflicts between the trustee and the beneficiary

- Restrictions that may frustrate beneficiaries seeking direct access to funds

- Limited protection against certain debts, such as child support or tax obligations

- Ongoing trustee fees for professional or institutional trustees

- Administrative responsibilities, such as accounting and tax filings

- Difficulty modifying terms after the trust is established

- Risk of poor trustee performance or misuse of discretion

- Delays in accessing funds when distributions are restricted

How Much Does a Spendthrift Trust Cost?

The cost of creating a spendthrift trust depends on several factors, including the complexity of the trust terms, the type and value of assets being transferred, and the number of beneficiaries involved. More detailed provisions or tax planning considerations can increase both the time and expense of drafting the trust. In addition, ongoing costs may arise if you hire a professional trustee to manage the trust or if the trust requires regular accounting and tax filings.

Because no two families have the same needs, it’s important to work with an experienced and knowledgeable Arizona estate planning attorney to determine the most appropriate structure for your family’s unique situation.

What Is the Process for Setting Up a Spendthrift Trust?

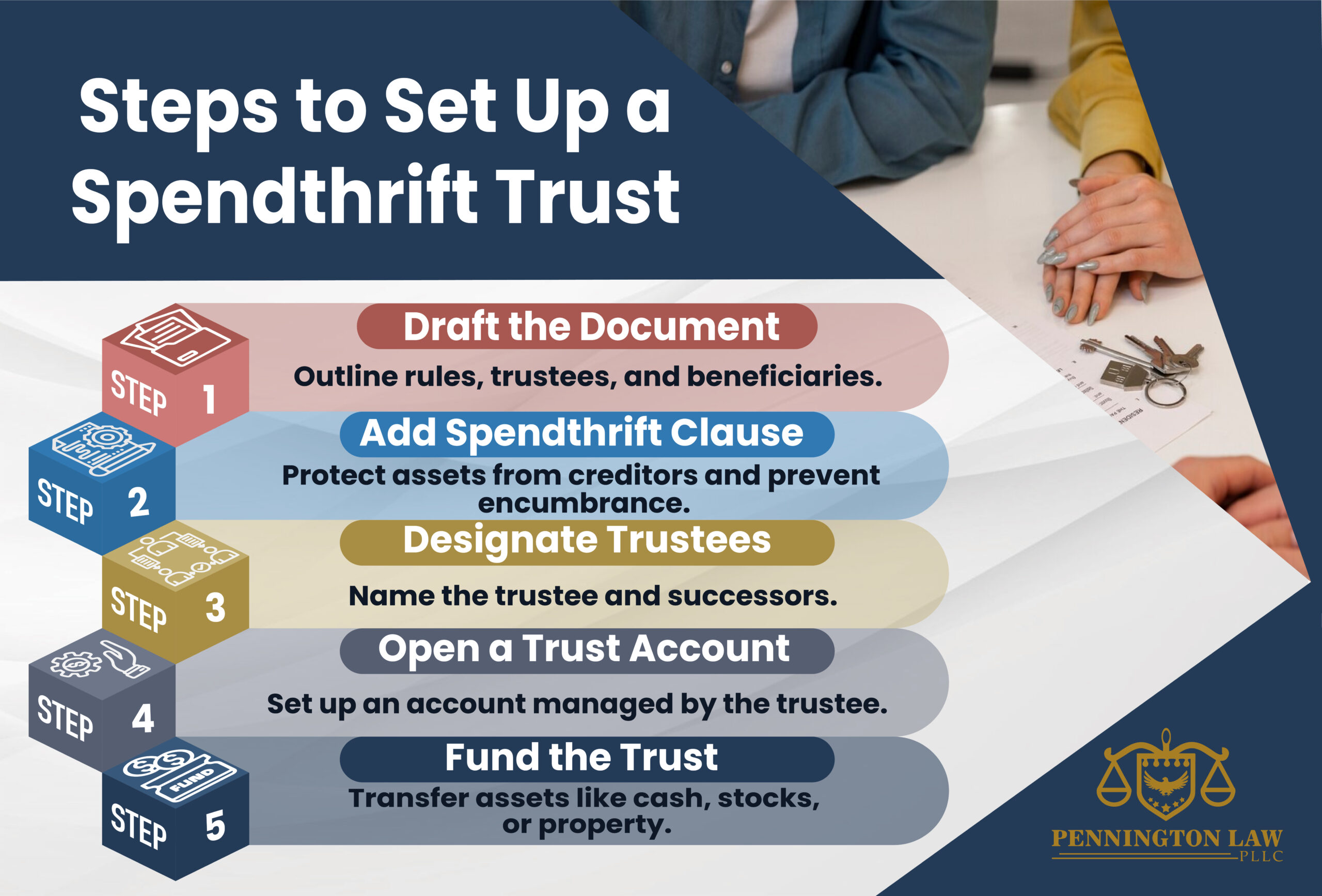

Setting up a spendthrift trust in Arizona involves several steps. First, you must write the spendthrift trust document that governs how the trust will operate. The trust document should name the trustee and any successor trustees and establish rules or guidelines for how the trustee should manage the trust. The trust should identify the beneficiary or beneficiaries.

The trust document should also include a spendthrift clause, which makes the trust a spendthrift trust. The spendthrift clause prohibits the beneficiary from encumbering future distributions from the trust, including borrowing against or pledging future distributions to creditors. The provision also expressly protects the trust assets and the beneficiary’s future distributions from creditors, meaning creditors cannot collect on the beneficiary’s debts from the spendthrift trust.

Once you have drafted and executed the trust document, you must set up a trust account at a bank or financial institution that the trustee controls. Then, you must fund the trust with money or other assets, such as stocks, bonds, annuities, or ownership of income properties.

Submit a Consultation Request form for spendthrift trust planning

Contact an Arizona Spendthrift Trust Lawyer Today

Over many years, Pennington Law, PLLC, has worked hard to protect the interests and wealth of families across Arizona. We strive to provide each client with tailored options that allow them to secure their assets and transfer them at the appropriate time. Our firm can help you pass your wealth on to your loved ones while protecting your estate from your heirs’ health problems, poor spending habits, or debts.

Let us help you safeguard your family’s financial future and provide you with peace of mind. Contact Pennington Law, PLLC, today for a free, no-obligation consultation to speak with an Arizona spendthrift trust attorney about your legal options and the suitability of a spendthrift trust for your estate plan.

Spendthrift Trusts Frequently Asked Questions

What does a spendthrift trust do?

People create spendthrift trusts to leave assets to a beneficiary while limiting the beneficiary’s access to them. This arrangement might be preferable if a family member suffers from substance abuse problems, a gambling addiction, or a tendency to overspend.

A spendthrift clause keeps ownership of the trust’s assets rather than transferring them outright at death. Distributions are made over time in accordance with terms set by the trustee. Because beneficiaries lack direct control, assets are generally insulated from creditor claims, lawsuits, and divorce proceedings (except for child support payments, government claims, or debts incurred before the trust was funded). This structure supports long-term management of funds while reducing risks associated with financial mismanagement for beneficiaries receiving structured assistance responsibly over extended periods.

How much does it cost to create a spendthrift trust?

The cost of creating a spendthrift trust varies based on factors such as trust complexity, asset type and value, and the number of beneficiaries. Detailed distribution terms or tax planning can increase drafting time and fees. Ongoing costs may also apply if a professional trustee is used or if accounting and tax filings are required. While attorney-drafted trusts involve higher initial fees, they are more likely to be properly executed and compliant with state and federal laws than DIY tools. A free consultation with an experienced trust lawyer lets you discuss your specific situation and receive a tailored estimate.

Can I change or update my spendthrift trust later?

Spendthrift trusts may be structured as revocable or irrevocable. A revocable spendthrift trust allows the grantor to modify terms or terminate the trust during their lifetime. This flexibility permits adjustments if a beneficiary’s circumstances change.

An irrevocable spendthrift trust generally offers greater protection from taxes and probate, but cannot be amended after creation. The choice depends on the desired balance between flexibility and permanence. The trust-maker selects whether the trust can be amended based on their asset protection needs and estate planning objectives.

How long does it take to set up a spendthrift trust?

Establishing a spendthrift trust requires careful planning and legal guidance. The process is similar to creating a standard trust but includes specific spendthrift provisions that define distribution schedules and limit a beneficiary’s access to trust assets. The time required to create the trust depends on factors such as its complexity and how quickly clients provide the necessary information during consultations and follow-ups.