Health care is one of the most significant expenses associated with aging. These costs can be sky-high if you experience an injury or illness that leaves you in need of long-term care. One method for paying for long-term care in Arizona is through Medicaid benefits. However, you may need to make careful estate planning decisions to qualify.

If the value of your assets makes you ineligible for Medicaid, placing some assets in a trust can help you qualify for benefits, but your choice of a trust will determine whether this approach is an option.

Is a Medicaid trust right for your needs? The Buckeye estate planning attorneys at Pennington Law, PLLC, can help you determine whether this is a viable strategy for your situation. Reach out for your free consultation today on Medicaid and revocable trusts.

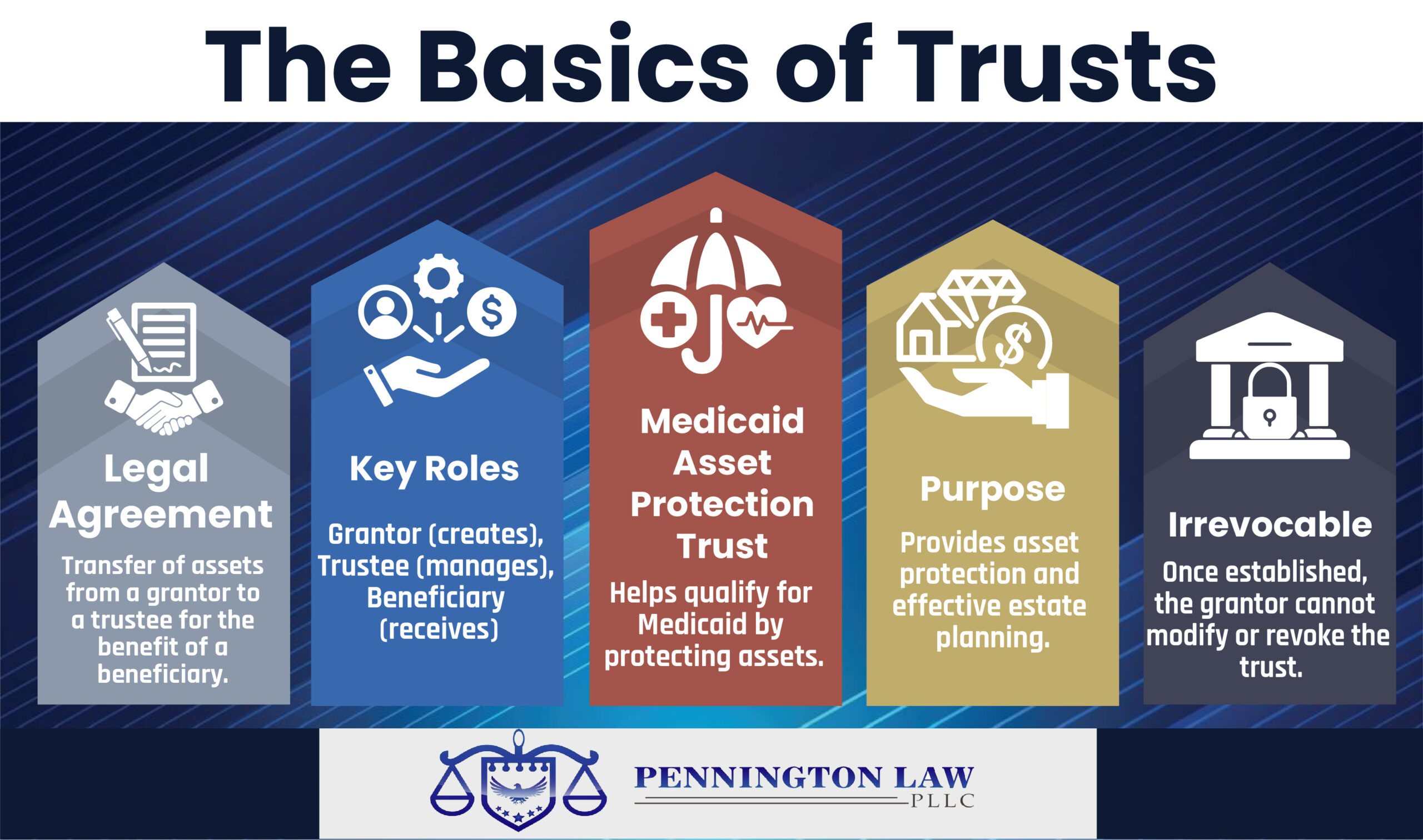

What is a Trust?

Trusts are legal agreements in which the owner of assets (the grantor) gives a third party (the trustee) the authority to oversee and manage assets on behalf of a beneficiary or a group of beneficiaries. Trusts are critical components of many estate plans because they offer long-term asset protection and a means of managing assets to benefit family members and other loved ones.

As a grantor ages, estate planning becomes essential for many reasons. Among them is the increased potential need for long-term care. Medicaid benefits can be helpful when paying for long-term care, but many people aren’t eligible for Medicaid due to the value of their assets.

For these individuals, Medicaid Asset Protection Trusts (MAPTs) offer an option to help them qualify for Medicaid benefits. Assets held in these irrevocable trusts are not counted for Medicaid eligibility purposes. MAPTs allow grantors to protect their assets and meet the eligibility requirements for Medicaid.

Revocable Trusts

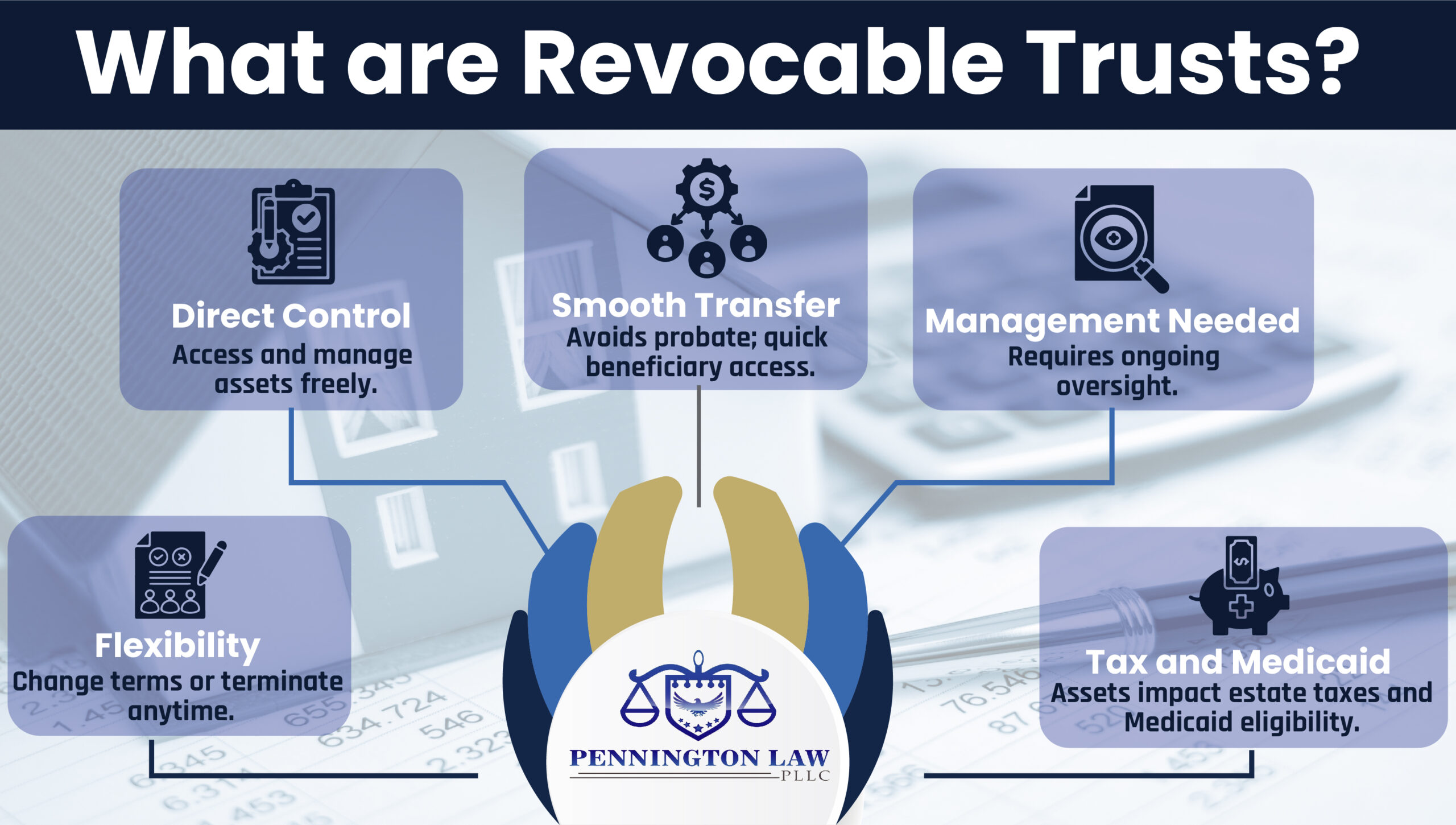

A revocable trust is a tool for estate planning and asset protection. It allows the grantor to manage and distribute their assets between selected trustees and beneficiaries throughout the owner’s life.

Some advantages of revocable trusts include the following:

- Flexibility – The grantor can change various elements of the trust’s terms, including beneficiaries and trustees, at any time. They also have the right to terminate the trust.

- Direct control – The grantor has free and direct control over the assets in a revocable trust, allowing them to access, add, or remove assets over time.

- Smooth asset transfer – Assets held in trust can transfer from grantor to beneficiary without going through probate, preventing potential delays and allowing beneficiaries to receive assets soon after the grantor’s death.

While some grantors feel more comfortable knowing they directly control their money and assets, there are some drawbacks to revocable trusts, including:

- Need for ongoing management – Grantors must manage their trusts consistently to ensure appropriate funding and address current and future concerns. Revocable trusts require frequent check-ins and thorough attention to detail. This option may not suit a grantor looking for limited involvement in their asset management.

- Tax consequences – Assets held in a revocable trust are part of the grantor’s estate. Because the grantor still has direct control over and access to their assets, the assets are not exempt from taxation following their death. Assets held in a revocable trust may also have to be used to pay off creditors.

- Medicaid implications – Because the grantor has direct access to their assets, revocable trusts can be used as an income source when the need for long-term care arises, which can render the grantor ineligible for Medicaid benefits.

Irrevocable Trusts

Some grantors prefer irrevocable trusts, especially for tax and Medicaid planning purposes. Irrevocable trusts have the inverse of many of a revocable trust’s critical features, including:

- Reduced control and flexibility – Once established, grantors cannot change an irrevocable trust, meaning they have no control over the held assets aside from what’s outlined in the trust agreement. Changing an established irrevocable trust requires approval from trustees and beneficiaries, making it much harder to modify than a revocable trust.

- More robust asset protection – Once put into the trust and under the trustee’s care, assets held in an irrevocable trust are not considered part of the grantor’s estate. This offers protection for those assets in various circumstances, including legal action and taxation.

- Medicaid planning benefits – Irrevocable trusts can help individuals preserve their assets and qualify for Medicaid benefits by removing a grantor’s direct access to their assets and transferring them to the trustee’s care. In other words, establishing a Medicaid trust in Arizona can positively affect your family’s future by helping you qualify for Medicaid without having to draw on protected assets.

Medicaid Implications for Arizona Residents

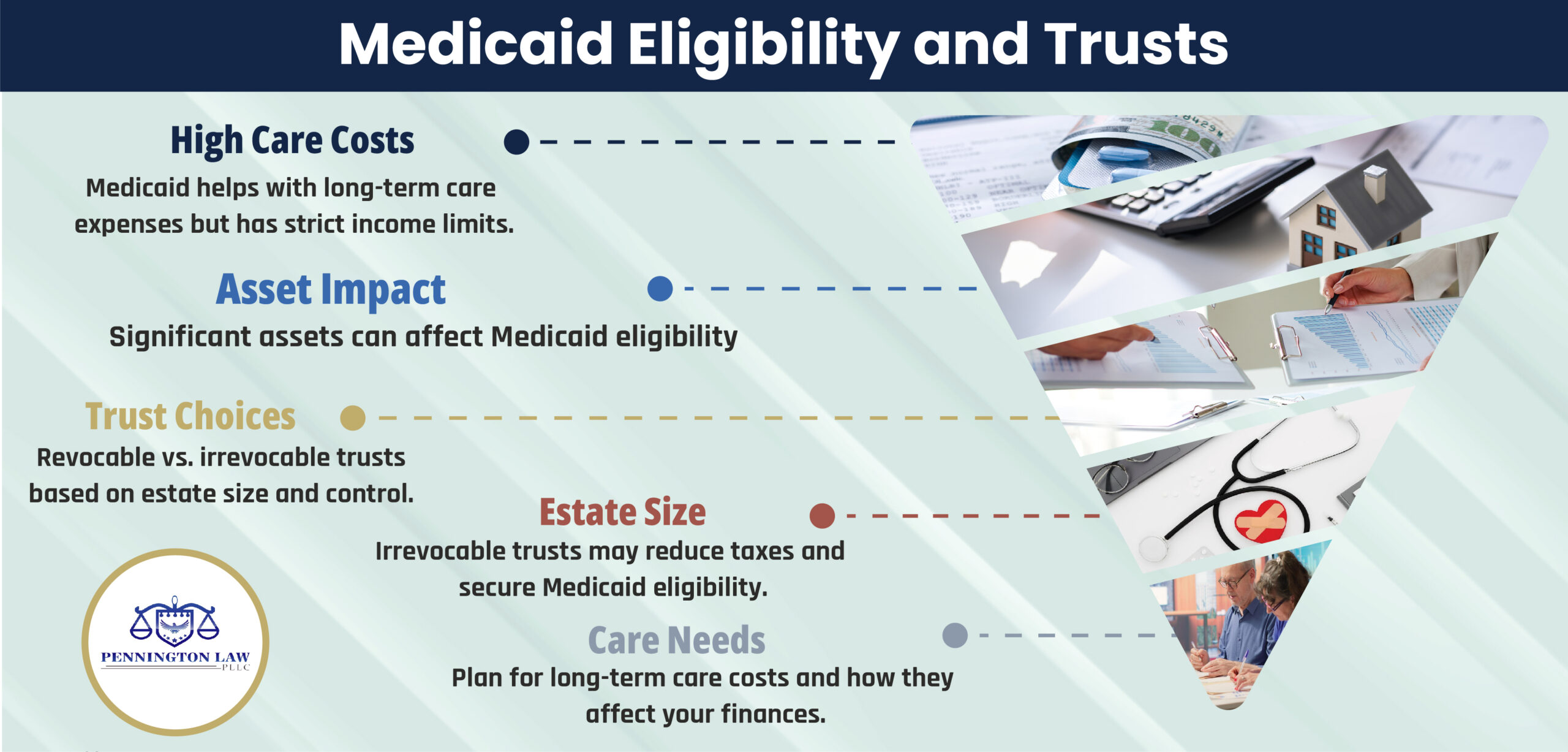

Given the potentially astronomical costs associated with long-term care, it makes sense to find ways to reduce the financial burden on your family while still having access to care if and when you need it. Medicaid can help but has strict eligibility requirements, including monthly income limits. If you have significant assets, you may not meet those requirements.

By familiarizing yourself with Medicaid eligibility requirements, you can make the financial and estate planning decisions today to help you secure the care you need without risking valuable assets and the legacy you leave behind.

When establishing a trust, you’ll want to choose an option that aligns best with your long-term goals and wishes for you and your beneficiaries. Crucial factors to consider when deciding between revocable and irrevocable trusts include:

- The value of your estate – An irrevocable trust may be best for larger estates, reducing tax expenses and securing Medicaid eligibility while protecting your assets.

- Desired control and flexibility – If you prefer to be in charge and enjoy the ability to update your estate to meet ever-changing needs, a revocable trust might be your preferred option.

- Medicaid planning goals – Consider how likely you are to require long-term care and the potential burden it might place on your finances. If you anticipate needing long-term care, don’t meet Medicaid eligibility requirements, and worry about those costs eating into your estate, an irrevocable trust can offer the protection you need while helping you qualify for Medicaid.

An experienced Medicaid trust lawyer can sit down with you and discuss what option might be best for your circumstances. Their perspective and guidance can help you find a solution that provides asset protection and valuable peace of mind.

Contact a Buckeye Estate Planning Lawyer Today

The best estate plan will address your needs, account for the unexpected, and protect you and your loved ones. If you have questions about long-term care and Medicaid planning and how they fit into your estate plan, a Buckeye Medicaid trust attorney can help. Contact Pennington Law, PLLC, today for a consultation with our experienced legal team.