Are you considering setting up an irrevocable life insurance trust (ILIT) but unsure of how to get it right? Taking the time to plan now could save your loved ones stress and money later. An Arizona estate planning lawyer from Pennington Law, PLLC can help you create an ILIT that fits your needs and complies with relevant laws.

Pennington Law, PLLC is a top-rated Arizona law firm focused on estate planning, trusts, wealth protection, and mo.re. Recognized by Super Lawyers and other peer-rated professional organizations, our mission is to protect your assets and create a lasting legacy for the ones you love. Contact us today to learn the benefits of a life insurance trust and how to get started.

What Is an ILIT Trust?

An irrevocable life insurance trust (ILIT) is a legal instrument that holds and controls a life insurance policy. The purpose of an ILIT is to keep the policy out of your estate for tax purposes. Because the trust owns the policy, the money from the life insurance policy doesn’t count toward your taxable estate. That can make a significant difference if your estate may face a substantial tax bill.

When you establish an ILIT trust, you appoint a trustee to manage the trust. You also choose beneficiaries who will receive the money from your life insurance policy after you die. Once you place a policy into the trust, you cannot withdraw it or modify the terms.

There are two types of ILITs:

- A funded ILIT includes other assets in the trust, such as cash or investments, from the start. These assets can cover the life insurance policy’s premiums.

- An unfunded ILIT only contains the life insurance policy. If you have an unfunded ILIT, you must make regular “gifts” to the trust so that the trustee has sufficient funds to pay the life insurance policy’s premiums.

How Does an Irrevocable Life Insurance Trust Work?

To create an ILIT, you typically begin by working with an experienced trusts and estates lawyer to draft the trust. You then apply for a life insurance policy. Importantly, the trust must own the policy, not you. Next, you make yearly gifts to the trust so it can pay the insurance premiums. The trustee uses those gifts to pay the premiums, not you. This keeps the policy separate from your taxable estate.

After you die, the insurance company pays the death benefit to the trust. Finally, the trustee follows your instructions and gives the money to your chosen beneficiaries. This setup avoids estate taxes on the insurance proceeds and can also protect the funds from creditors.

Five Elements to Consider When Making an ILIT

Before creating an ILIT, you should take the time to understand how it works and what you must relinquish. An ILIT can reduce estate taxes and protect life insurance money for your family, but you must take care in creating and managing the trust.

For instance, you’ll need to make annual gifts to the trust so it can pay insurance premiums. The trustee must also send Crummey letters each year to let the beneficiaries know about those gifts. These letters help the gifts qualify for the annual gift tax exclusion.

You also need to follow other best practices, such as selecting the right trustee and establishing the trust before applying for the policy. When you plan ahead, an ILIT can offer long-term value in your estate plan.

Here are five additional elements to consider if you choose to create an ILIT:

1. ILITs Can Grant You Distributions, But You Can’t Be a Trustee or Beneficiary

You can’t name yourself as the trustee or a beneficiary of your ILIT or have any direct control over the trust once it’s set up. If you do, the IRS will likely include the value of the life insurance policy in your taxable estate, which defeats the purpose of the trust. However, your trustee may use the trust funds to support your needs in certain ways, depending on how you write the trust terms.

2. Be Aware of IRS “Step Transaction” Challenges

If you set up an ILIT and transfer a life insurance policy to it too soon after creating the trust, the IRS might treat the actions as one single event. This is known as a “step transaction.” If that happens, you could lose the tax benefit you wanted. You can avoid this by creating the trust first and then applying for a new life insurance policy in the trust’s name.

3. Understand That Irrevocable Trusts Can’t Be Changed

Once you sign the trust, you can’t change it. You can’t take the policy back, add new terms, or remove a beneficiary. That’s why you must feel confident in your choices and get things right the first time. Make sure your trustee understands your wishes and that the trust includes clear instructions.

4. Keep the Three-Year Rule in Mind

If you die within three years of moving a life insurance policy into the trust, the IRS might still count the policy as part of your estate. However, this rule doesn’t apply if the trust owns the policy from the start.

5. Remember the Benefits of ILITs

Among the benefits of an irrevocable life insurance trust is that it can lower estate taxes, protect life insurance money from creditors, and give you more control over how that money helps your family. When you set up an ILIT correctly, it can be a highly beneficial part of your estate plan.

How an Arizona Trust Administration Lawyer Can Help

Creating an effective ILIT takes more than filling out a few forms. You must follow detailed rules to receive the tax benefits and ensure the trust operates as intended. An experienced trust administration attorney can guide you through the entire process and advise you of your various options and their pros and cons.

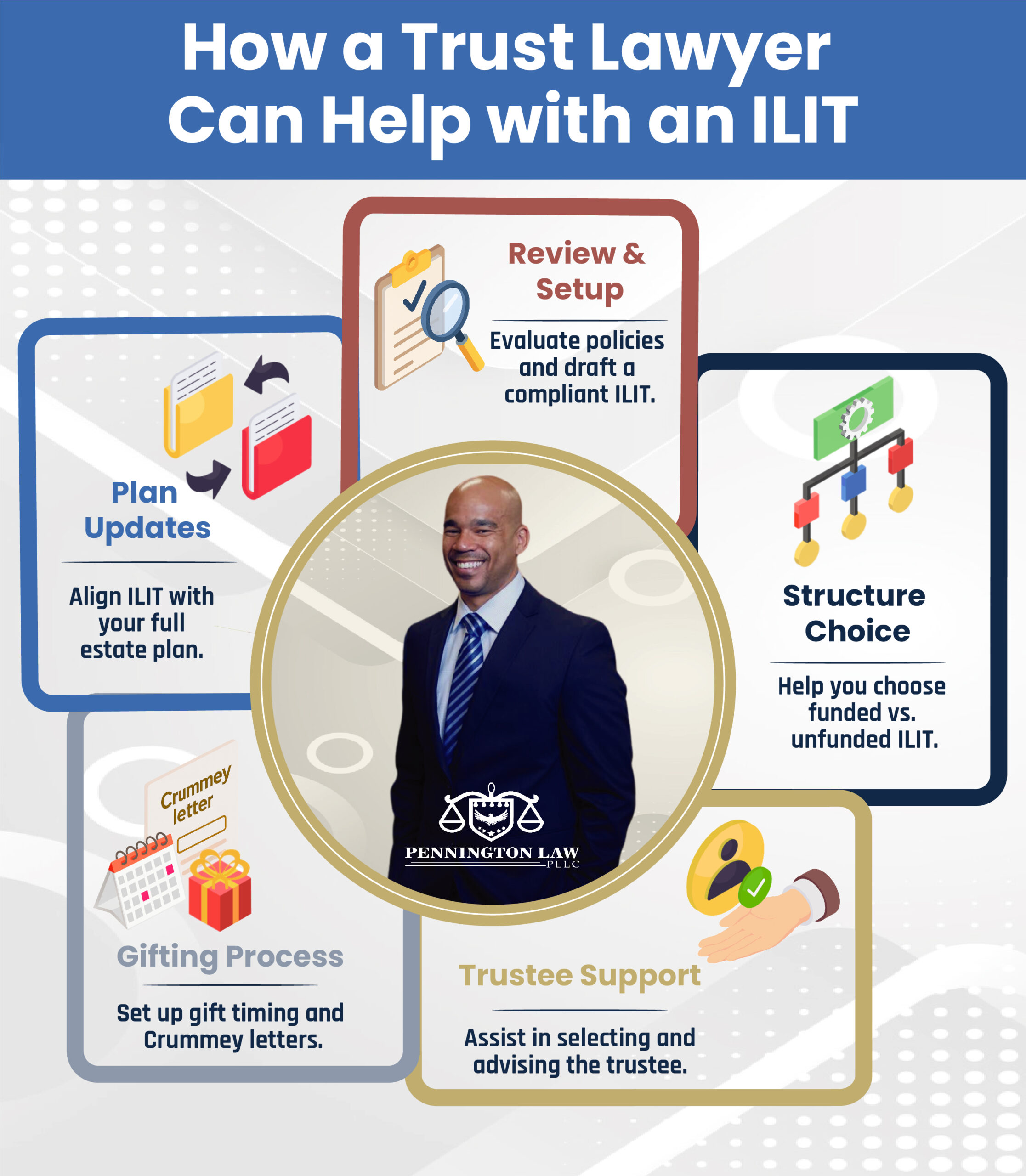

At Pennington Law, PLLC, we can provide guidance by:

- Reviewing current life insurance policies and explaining which ones could work with an ILIT

- Helping you decide whether to create a funded or unfunded ILIT

- Drafting clear trust documents that follow IRS rules and match your goals

- Assisting you in choosing the right trustee and making sure they understand their duties

- Discussing how irrevocable life insurance trust premium payments are handled

- Setting up the timing and process for gifting money into the trust each year

- Preparing Crummey letters for your trustee to send to the beneficiaries

- Planning the ILIT structure to avoid mistakes that trigger estate taxes

- Updating your overall estate plan to reflect the new ILIT

- Guiding your family members on how to manage the ILIT after your death

Contact Pennington Law, PLLC for a Complimentary Consultation

If you’re exploring options to enhance your estate plan and limit tax consequences, an ILIT could be part of your solution. Contact an experienced Arizona trusts lawyer at Pennington Law, PLLC to get started with a free consultation. We can answer your questions, explain your options, and help you take your next steps with confidence.