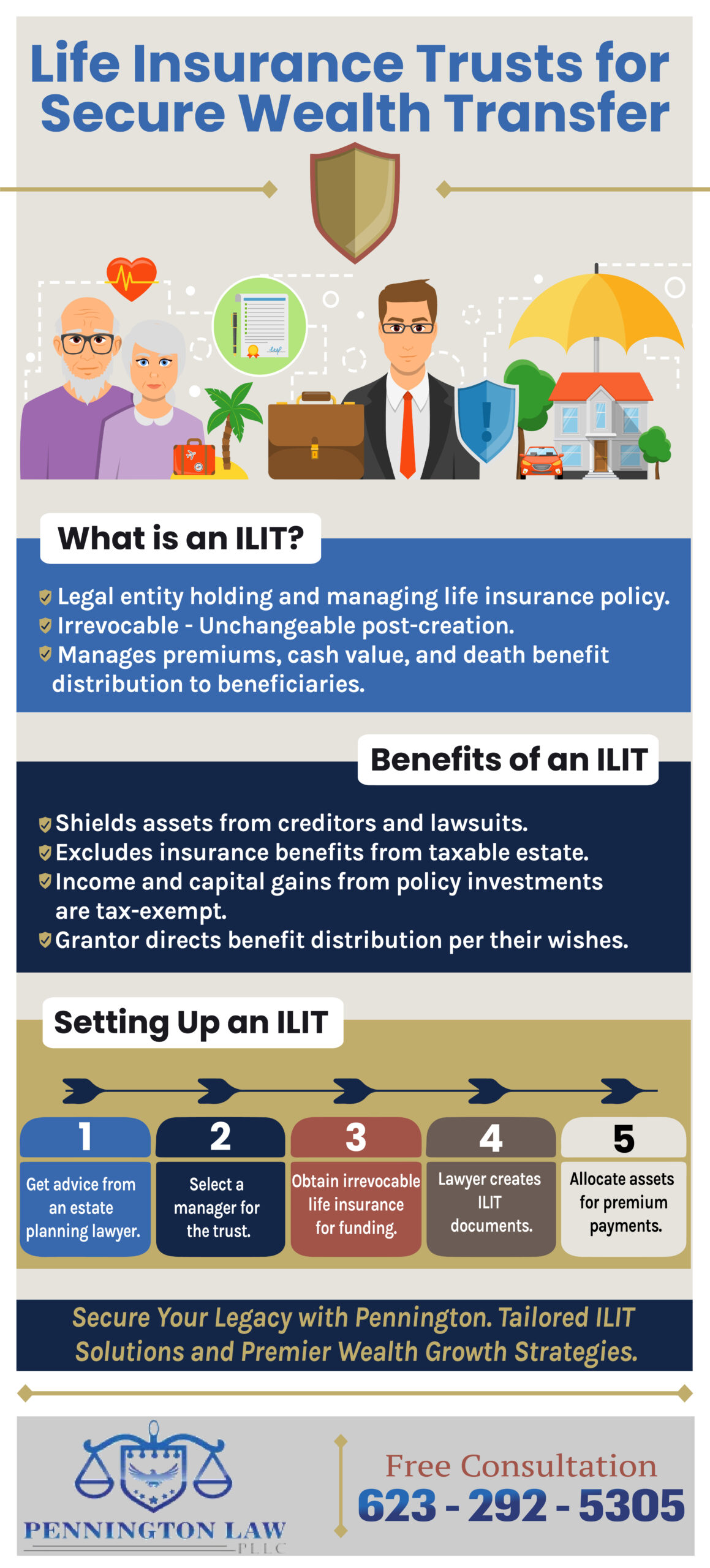

An irrevocable life insurance trust (ILIT) is a particular type of trust designed to protect and control term and permanent life insurance policies while the insured person is still alive. ILITs have several advantages, including providing tax-free death benefits and safeguarding the insurance policy from creditors and divorce.

![]()

If you’re considering setting up an irrevocable trust for your heirs, seek the help of a qualified estate planning attorney with Pennington Law, PLLC. We can provide valuable guidance and advice as we establish the ILIT to your wishes. We can also help you select a suitable trustee, prepare trust documents, and integrate your ILIT into a broader estate plan.

Our estate planning attorneys are standing by to protect your wishes and safeguard your future. Contact us today for a free ILIT consultation with an irrevocable life insurance trusts lawyer in West Valley Arizona.

Who Should Consider an ILIT?

Now that you know what an ILIT is, you might wonder whether it’s right for you. You should consider establishing an ILIT if:

- You Have a Considerable Net Worth – Those who have at least $5 million and hold permanent life insurance policies stand to benefit most from an ILIT.

- You Own a Business – If most of your assets are tied up in your business, an ILIT can prevent your heirs from having to sell part or all of your company to pay estate taxes.

- You Work in a Field That Makes You Vulnerable to Lawsuits – Doctors, attorneys, and other professionals who might be the target of a lawsuit can protect their assets from creditors and judgments by placing them in an irrevocable trust.

The best way to decide is to talk to an experienced Arizona estate planning attorney.